Flow from IRP to GST System/E-Way Bill System & Buyer

Part B: Flow from IRP to GST System/E-Way Bill System & Buyer

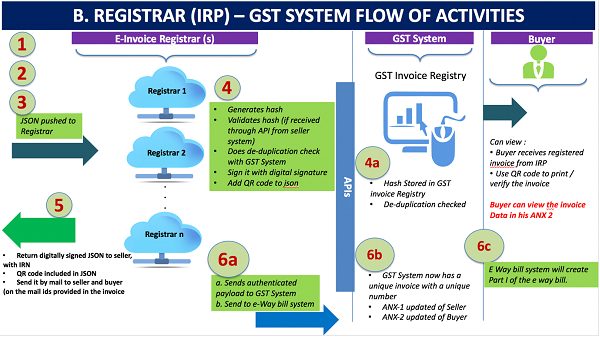

The following diagram shows how e-Invoice data would be consumed by GST System for generation of e-way bill or populating relevant parts GST Returns, stated in Step-5 above.

Step 5(a) will be to share the signed e-invoice data along with IRN (same as that has been returned by the IRP to the seller) to the GST System as well as to E-Way Bill System.

Step 5b The GST System will update the ANX-1 of the seller and ANX-2 of the buyer, which in turn will determine liability and ITC.

Step 5c E-Way bill system will create Part-A of e-way bill using this data to which only vehicle number will have to be attached in Part-B of the e-way bill.

Note 1: The e-invoice standardized schema has mandatory and optional items. The e-invoice shall not be accepted in the GST System unless all the mandatory items are present. The optional items are to be used by the seller and buyer as per their business need to enforce their business obligations or relationships.

Note 2: Seller may send his e-invoice for registration to more than one registrar. But the GST system and IRP will perform a de-duplication check with central registry to ensure that the IRN that is generated is unique for each invoice. Therefore, the IRP shall return ONLY ONE registered IRN for each invoice to the seller. In case of multiple registrars (more than one IRPs) only one IRP will return a valid IRN to the seller. Except one, all other IRPs will reject the request of registration.

Note 3: The QR code will enable quick view, validation and access of the invoices from the GST system from hand held devices.