While the word invoice is used in the name of e-invoice, it covers other documents that will be required to be reported to IRP by the creator of the document:

i. Invoice by Supplier

ii. Credit Note by Supplier

iii. Debit Note by Recipient

iv. Any other document as required by law to be reported by the creator of the document

What will be the workflow involved?

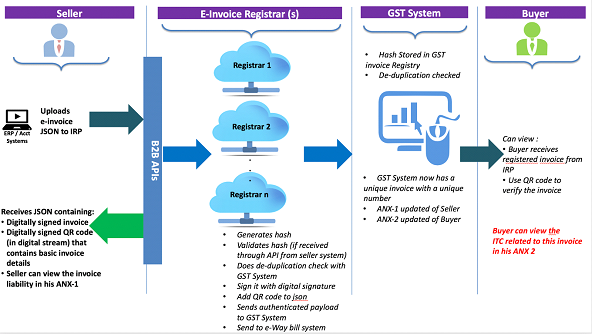

The flow of the e-invoice generation, registration and receipt of confirmation can be logically divided into two major parts.

a) The first part being the interaction between the business (supplier in case of invoice) and the Invoice Registration Portal (IRP).

b) The second part is the interaction between the IRP and the GST/E-Way Bill Systems and the Buyer.

The two parts of the workflow are depicted diagrammatically below and followed up with an explanation of the steps involved. As the process evolves and system matures the same would be intercommunicated between buyer’s software and seller’s software, banking systems etc.

The contents of Documents are to be reported to GST System